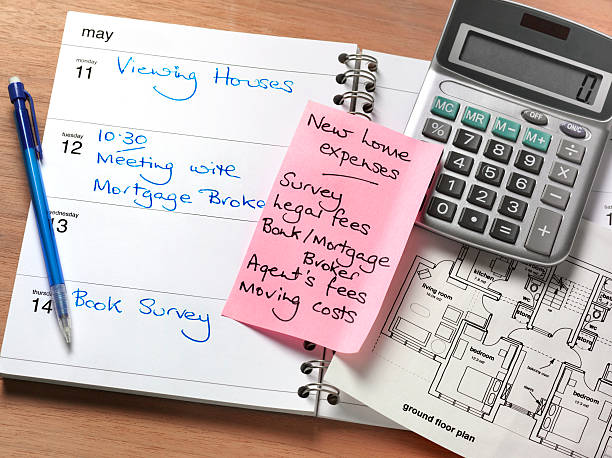

As a homeowner, your monthly mortgage payment is a major part of your budget. But it’s not the only cost of owning your home. A smart homeowner knows to plan for the ongoing care their property needs. This is where a maintenance cost estimate comes in. Think of it as a yearly budget for keeping your home safe, functional, and valuable. It’s not about flashy renovations; it’s about the essential upkeep that prevents small problems from becoming expensive disasters. So, what exactly is included in this estimate? Let’s break it down into the key areas you should consider.First and foremost, a good maintenance estimate includes routine servicing for your home’s major systems. Your heating and air conditioning units need regular check-ups, typically once a year, to run efficiently and avoid a costly mid-winter breakdown. Similarly, your water heater has parts that wear out and may need flushing to remove sediment. These are predictable costs you can schedule and save for. Another critical system is your plumbing. While a leaky faucet might seem minor, the estimate should account for fixing drips, clearing slow drains, and checking for hidden leaks that can cause water damage or mold. Electrical system checks, like ensuring your outlets are safe and your electrical panel is in good order, also fall under this preventative umbrella.The exterior of your home is its first line of defense against the elements, so a significant portion of your maintenance budget should be dedicated to its care. This includes your roof. Even a long-lasting roof will eventually need repairs to shingles or flashing, and you should be setting aside money for its eventual full replacement. Your home’s siding or paint requires periodic cleaning, touch-ups, or repainting to protect the structure underneath. Gutters and downspouts are easily forgotten but crucial; they should be cleaned at least twice a year to prevent water from pooling around your foundation, which can lead to serious structural issues. Don’t forget about windows and doors—resealing them improves energy efficiency and keeps moisture out.The landscape and outdoor areas are more than just curb appeal; they are part of your home’s health. Your estimate should include basic lawn care like mowing and seasonal fertilization if you do it yourself or hire a service. Trees need occasional trimming, especially branches that hang over your roof or could fall in a storm. If you have a deck or patio, it will need to be cleaned, sealed, or stained every few years to prevent rot and splintering. Driveways and walkways may develop cracks that need sealing to keep them from worsening. These items protect your property value and prevent safety hazards.Inside your home, wear and tear is a constant factor. Walls get scuffed, floors get scratched, and caulking in bathrooms and kitchens dries out and cracks. Your maintenance fund should cover the cost of fresh paint, floor refinishing, and re-caulking tubs and showers to prevent water from seeping into walls. Appliances, while not always considered “maintenance,“ have a limited lifespan. Setting aside money for the eventual repair or replacement of your refrigerator, dishwasher, or washing machine is a prudent part of homeownership. It’s also wise to include a line item for pest control, whether it’s an annual termite inspection or dealing with occasional invaders.Finally, and perhaps most importantly, a realistic maintenance cost estimate must include an emergency fund. No matter how well you plan, unexpected things happen. A pipe might burst in the middle of the night, a storm could damage your fence, or your furnace could fail on the coldest day of the year. Experts often recommend saving one to three percent of your home’s purchase price each year for maintenance and repairs. For a newer home, you might lean toward the lower end; for an older home with more character (and more potential issues), you should aim for the higher end. By setting this money aside consistently, you turn a potential financial crisis into a manageable inconvenience.In the end, creating a maintenance cost estimate is an act of responsibility and care for your biggest investment. It moves you from reacting to problems in a panic to proactively preserving your home’s comfort and value. When you combine your mortgage payment with a solid maintenance plan, you get a true picture of the cost of homeownership—and the peace of mind that comes with being truly prepared.

As a homeowner, your monthly mortgage payment is a major part of your budget. But it’s not the only cost of owning your home. A smart homeowner knows to plan for the ongoing care their property needs. This is where a maintenance cost estimate comes in. Think of it as a yearly budget for keeping your home safe, functional, and valuable. It’s not about flashy renovations; it’s about the essential upkeep that prevents small problems from becoming expensive disasters. So, what exactly is included in this estimate? Let’s break it down into the key areas you should consider.First and foremost, a good maintenance estimate includes routine servicing for your home’s major systems. Your heating and air conditioning units need regular check-ups, typically once a year, to run efficiently and avoid a costly mid-winter breakdown. Similarly, your water heater has parts that wear out and may need flushing to remove sediment. These are predictable costs you can schedule and save for. Another critical system is your plumbing. While a leaky faucet might seem minor, the estimate should account for fixing drips, clearing slow drains, and checking for hidden leaks that can cause water damage or mold. Electrical system checks, like ensuring your outlets are safe and your electrical panel is in good order, also fall under this preventative umbrella.The exterior of your home is its first line of defense against the elements, so a significant portion of your maintenance budget should be dedicated to its care. This includes your roof. Even a long-lasting roof will eventually need repairs to shingles or flashing, and you should be setting aside money for its eventual full replacement. Your home’s siding or paint requires periodic cleaning, touch-ups, or repainting to protect the structure underneath. Gutters and downspouts are easily forgotten but crucial; they should be cleaned at least twice a year to prevent water from pooling around your foundation, which can lead to serious structural issues. Don’t forget about windows and doors—resealing them improves energy efficiency and keeps moisture out.The landscape and outdoor areas are more than just curb appeal; they are part of your home’s health. Your estimate should include basic lawn care like mowing and seasonal fertilization if you do it yourself or hire a service. Trees need occasional trimming, especially branches that hang over your roof or could fall in a storm. If you have a deck or patio, it will need to be cleaned, sealed, or stained every few years to prevent rot and splintering. Driveways and walkways may develop cracks that need sealing to keep them from worsening. These items protect your property value and prevent safety hazards.Inside your home, wear and tear is a constant factor. Walls get scuffed, floors get scratched, and caulking in bathrooms and kitchens dries out and cracks. Your maintenance fund should cover the cost of fresh paint, floor refinishing, and re-caulking tubs and showers to prevent water from seeping into walls. Appliances, while not always considered “maintenance,“ have a limited lifespan. Setting aside money for the eventual repair or replacement of your refrigerator, dishwasher, or washing machine is a prudent part of homeownership. It’s also wise to include a line item for pest control, whether it’s an annual termite inspection or dealing with occasional invaders.Finally, and perhaps most importantly, a realistic maintenance cost estimate must include an emergency fund. No matter how well you plan, unexpected things happen. A pipe might burst in the middle of the night, a storm could damage your fence, or your furnace could fail on the coldest day of the year. Experts often recommend saving one to three percent of your home’s purchase price each year for maintenance and repairs. For a newer home, you might lean toward the lower end; for an older home with more character (and more potential issues), you should aim for the higher end. By setting this money aside consistently, you turn a potential financial crisis into a manageable inconvenience.In the end, creating a maintenance cost estimate is an act of responsibility and care for your biggest investment. It moves you from reacting to problems in a panic to proactively preserving your home’s comfort and value. When you combine your mortgage payment with a solid maintenance plan, you get a true picture of the cost of homeownership—and the peace of mind that comes with being truly prepared.

A recast directly changes your amortization schedule. After the lump-sum payment is applied, the lender creates a brand-new schedule that spreads the remaining principal balance (plus interest) evenly over the remaining loan term. This results in a lower portion of each future payment going toward interest and a higher portion going toward principal than in your original schedule at the same point in time.

A third mortgage is a subordinate loan taken out on a property that already has a first and a second mortgage. It is a type of home equity loan, but it sits in third-lien position, meaning it gets paid back only after the first and second mortgages are satisfied in the event of a foreclosure.

Open Market Operations are the Fed’s daily buying and selling of U.S. government securities (like Treasury bonds) in the open market. To influence rates downward, the Fed buys securities, which adds money to the banking system. To push rates upward, it sells securities, pulling money out of the system. This is the primary mechanism for keeping the Federal Funds Rate near its target.

Yes, jumbo loan refinancing is available. You can refinance to lower your interest rate, change your loan term, or take cash out (though cash-out refinances on jumbo loans have very strict limits and requirements). The qualification process for a jumbo refinance is just as rigorous as for a purchase loan.

You can access your home’s equity through several loan products, primarily a Home Equity Loan, a Home Equity Line of Credit (HELOC), or a Cash-Out Refinance. These options allow you to borrow against the equity you’ve built up, providing a lump sum or a flexible line of credit to fund your improvement projects.