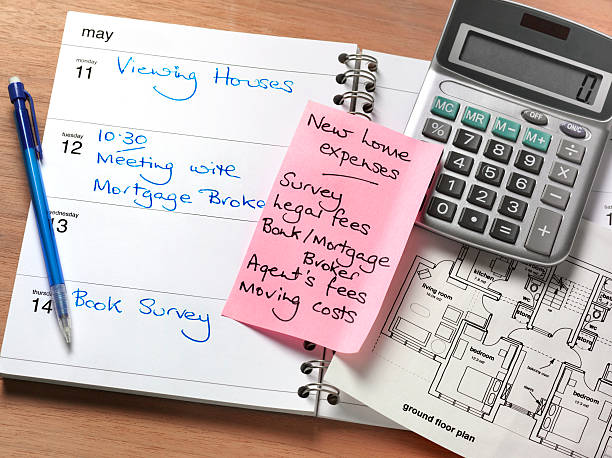

When you decide to take out a cash-out refinance on your home, you are often doing so to free up equity for a specific purpose—like a major home renovation. It is an exciting way to breathe new life into your living space, add comfort, or increase the future value of your property. However, once the cash is in your bank account, the real work begins. Managing a home improvement project can quickly become overwhelming if you do not have a clear plan. Costs often spiral due to unexpected repairs, changes in design, or simply losing track of small, recurring expenses.Successful renovations rely on disciplined budgeting and organization from day one. You need to know exactly how much you are spending on materials, contractor fees, permits, and those inevitable “just in case” funds for surprises behind the walls. By using a dedicated system to track every dollar, you protect the investment you made by refinancing your home. It keeps you focused on your goals, prevents you from overextending your finances, and ensures that you finish the project with the home improvements you envisioned rather than a half-finished space and an empty wallet. Before you start pulling down drywall, make sure you have the right tools to keep your project finances organized and transparent throughout the entire renovation process.This planner is an excellent choice for homeowners who prefer a physical, hands-on way to manage their renovation finances. Measuring 8.5 by 11 inches, it provides plenty of space to write down detailed project costs. It serves as a comprehensive log for everything from expensive hardware to small supplies that can sneakily add up over time. By keeping all your receipts and price quotes in one place, you significantly reduce the stress of managing a large-scale project. It is specifically designed to help you maintain a clear view of your budget, ensuring you stay on track throughout your remodel.If you are looking for more than just a ledger, this all-in-one planner is a fantastic companion for your home improvement journey. Beyond simple budget tracking, it includes sections for project checklists and sketches, which are vital for organizing your ideas and ensuring your vision remains consistent. Renovations often involve juggling multiple tasks simultaneously, and this journal helps you stay coordinated. It acts as a project diary, helping you monitor your progress room by room. It is a practical tool for keeping your renovation organized, preventing costly mistakes, and ensuring that your home improvement project stays on schedule and budget.Keeping your spending under control is the most challenging part of any renovation, and this dedicated logbook is designed to make that job easier. It is structured to help you categorize your expenses, making it simple to see where your money is going at any point in the project. Whether you are tackling a minor update or a total kitchen gut, this tracker helps you avoid the common trap of overspending. By regularly recording your transactions, you create a clear roadmap that alerts you if you are straying from your financial plan, allowing you to make necessary adjustments early.This specialized tracker offers a professional-grade approach to managing your renovation finances. It includes useful features such as contractor comparison forms, which help you ensure you are getting the best value for your money. With 20 weeks of project logs and detailed, room-by-room cost breakdowns, it provides a structured way to handle complex remodels. It also includes sections for tracking payments, which is essential for managing your cash flow. If you have used a cash-out refinance to fund your project, this tool is ideal for ensuring you maximize those funds and bring your renovation goals to life efficiently.

When you decide to take out a cash-out refinance on your home, you are often doing so to free up equity for a specific purpose—like a major home renovation. It is an exciting way to breathe new life into your living space, add comfort, or increase the future value of your property. However, once the cash is in your bank account, the real work begins. Managing a home improvement project can quickly become overwhelming if you do not have a clear plan. Costs often spiral due to unexpected repairs, changes in design, or simply losing track of small, recurring expenses.Successful renovations rely on disciplined budgeting and organization from day one. You need to know exactly how much you are spending on materials, contractor fees, permits, and those inevitable “just in case” funds for surprises behind the walls. By using a dedicated system to track every dollar, you protect the investment you made by refinancing your home. It keeps you focused on your goals, prevents you from overextending your finances, and ensures that you finish the project with the home improvements you envisioned rather than a half-finished space and an empty wallet. Before you start pulling down drywall, make sure you have the right tools to keep your project finances organized and transparent throughout the entire renovation process.This planner is an excellent choice for homeowners who prefer a physical, hands-on way to manage their renovation finances. Measuring 8.5 by 11 inches, it provides plenty of space to write down detailed project costs. It serves as a comprehensive log for everything from expensive hardware to small supplies that can sneakily add up over time. By keeping all your receipts and price quotes in one place, you significantly reduce the stress of managing a large-scale project. It is specifically designed to help you maintain a clear view of your budget, ensuring you stay on track throughout your remodel.If you are looking for more than just a ledger, this all-in-one planner is a fantastic companion for your home improvement journey. Beyond simple budget tracking, it includes sections for project checklists and sketches, which are vital for organizing your ideas and ensuring your vision remains consistent. Renovations often involve juggling multiple tasks simultaneously, and this journal helps you stay coordinated. It acts as a project diary, helping you monitor your progress room by room. It is a practical tool for keeping your renovation organized, preventing costly mistakes, and ensuring that your home improvement project stays on schedule and budget.Keeping your spending under control is the most challenging part of any renovation, and this dedicated logbook is designed to make that job easier. It is structured to help you categorize your expenses, making it simple to see where your money is going at any point in the project. Whether you are tackling a minor update or a total kitchen gut, this tracker helps you avoid the common trap of overspending. By regularly recording your transactions, you create a clear roadmap that alerts you if you are straying from your financial plan, allowing you to make necessary adjustments early.This specialized tracker offers a professional-grade approach to managing your renovation finances. It includes useful features such as contractor comparison forms, which help you ensure you are getting the best value for your money. With 20 weeks of project logs and detailed, room-by-room cost breakdowns, it provides a structured way to handle complex remodels. It also includes sections for tracking payments, which is essential for managing your cash flow. If you have used a cash-out refinance to fund your project, this tool is ideal for ensuring you maximize those funds and bring your renovation goals to life efficiently.

A recast and a refinance are fundamentally different. A recast keeps your existing loan intact—same lender, interest rate, and loan term—and only lowers your monthly payment by re-amortizing the principal. A refinance replaces your old loan with an entirely new one, which can change your interest rate, term, and monthly payment, but it involves credit checks, closing costs, and fees, unlike a simple recast.

Yes, indirectly. A higher credit score can sometimes help you qualify for a loan with a lower down payment. For example, with a strong credit profile, you might be approved for a conventional loan with just 3% down. With a lower score, a lender may require a larger down payment (e.g., 10-20%) to reduce their risk, which lowers your loan-to-value (LTV) ratio.

Congratulations! With your largest monthly expense gone, you can:

Supercharge your retirement and investment accounts.

Save for other large goals, like college funds or a vacation property.

Build a more substantial cash cushion.

Enjoy the financial security and peace of mind that comes with owning your home free and clear.

Yes, but only if the loan was used to “buy, build, or substantially improve” the home that secures the loan. The debt must also fall within the $750,000 (or $1 million) total mortgage limit. You cannot deduct interest on a home equity loan used for personal expenses, such as paying off credit card debt or funding a vacation.

Mortgage insurance protects the lender—not you—in case you default on your loan. It is typically required on conventional loans with a down payment of less than 20% (called Private Mortgage Insurance or PMI) and is always required on FHA loans (as an Upfront and Annual Mortgage Insurance Premium).