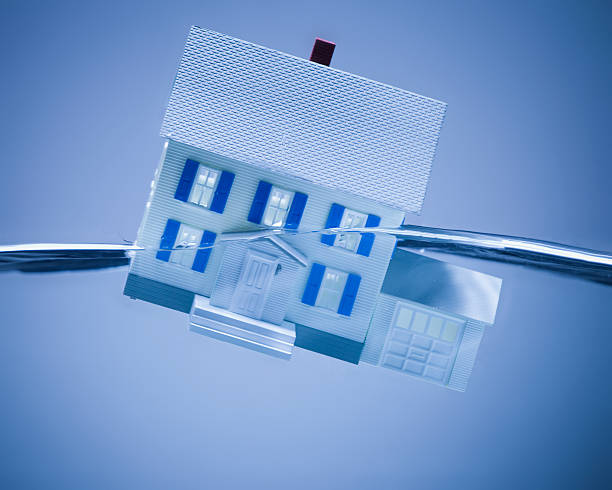

If you have owned a home for a few years, you have probably heard a lot about home equity. It is the difference between what your home is worth and what you still owe on your mortgage. Many homeowners see equity as a pile of cash they can use for renovations, debt repayment, or even a new car. Tapping into that equity through a second mortgage or a home equity line of credit can feel like free money. But there is a risk that does not get talked about enough: what happens when home prices drop.Home values do not always go up. In some years they go sideways, and in others they fall sharply. If you have borrowed against your equity and then the market turns, you can find yourself in a very difficult spot. This is one of the biggest risks of leveraging your home equity, yet many people do not think about it until it is too late.When you take out a second mortgage or a home equity line of credit, you are using your home as collateral. That means if you stop paying, the lender can take your house. But even if you keep making every payment on time, a drop in home value can still cause trouble. Imagine your home is worth three hundred thousand dollars and you owe two hundred thousand on your first mortgage. That leaves you with one hundred thousand in equity. You decide to take out a home equity line of credit for fifty thousand dollars to remodel your kitchen. Now your total debt is two hundred and fifty thousand dollars. Your equity is down to fifty thousand dollars. That still seems safe enough.Then the market takes a downturn. Home values in your neighborhood fall by twenty percent. Your three hundred thousand dollar home is now worth two hundred and forty thousand dollars. But you still owe two hundred and fifty thousand. You owe more than the house is worth. You are underwater. This is also called negative equity.Being underwater does not automatically mean you will lose your home. If you keep making payments, your lender will not take any action. But the problem comes when something changes in your life. Maybe you lose your job, get divorced, or need to move for a new job. You cannot sell your home without bringing cash to the closing table to pay off the difference between what the house sells for and what you owe. That can be tens of thousands of dollars that you may not have.Another problem is that your home equity line of credit may be frozen or reduced. Many lenders have the right to lower your credit limit or stop you from drawing more money if the value of your home falls. That can catch you off guard if you were counting on that money for an emergency or a planned expense. You might have already used part of the line, but the remaining available credit disappears.A drop in home value also makes it harder to refinance. If you want to lower your interest rate or switch from an adjustable rate to a fixed rate, you need enough equity to qualify. When home prices fall, you may not have that equity. You could be stuck with a higher payment or a loan that is about to adjust upward.There is also the stress factor. Knowing that you owe more than your home is worth can feel like a weight. It can affect your decisions about upgrades, moving, or even taking on new debt. Some people panic and try to sell at a loss, while others hold on hoping the market will come back. That wait can last years. In some housing downturns, it took a decade for prices to recover.The best way to protect yourself is to be conservative when using your home equity. Do not borrow the maximum amount you are offered. Leave a cushion. Think about what would happen if your home value dropped by ten or fifteen percent. Would you still have some equity left? If not, you are too close to the edge.Also remember that a home is a place to live, not an ATM. Using your equity for expenses that do not add lasting value, like vacations or a new car, can leave you with debt and no way to pay it back if the market turns. Even if you use the money for home improvements, make sure those improvements actually increase the value of your house by at least as much as you borrow. Not all renovations pay off.Finally, keep an eye on your local housing market. If prices in your area have been climbing fast for a few years, a correction may be overdue. That is not a reason to panic, but it is a reason to be extra careful about how much equity you take out. A downturn can happen quickly, and once you have borrowed against your home, you cannot undo that decision.Leveraging your home equity can be a useful tool. But it comes with real risk. The biggest risk is that home values do not always go up. When they fall, the equity you thought was yours can disappear, and you could end up owing more than your house is worth. That is a situation no homeowner wants to face. By understanding this risk ahead of time, you can make smarter choices about how much equity to use and when.

If you have owned a home for a few years, you have probably heard a lot about home equity. It is the difference between what your home is worth and what you still owe on your mortgage. Many homeowners see equity as a pile of cash they can use for renovations, debt repayment, or even a new car. Tapping into that equity through a second mortgage or a home equity line of credit can feel like free money. But there is a risk that does not get talked about enough: what happens when home prices drop.Home values do not always go up. In some years they go sideways, and in others they fall sharply. If you have borrowed against your equity and then the market turns, you can find yourself in a very difficult spot. This is one of the biggest risks of leveraging your home equity, yet many people do not think about it until it is too late.When you take out a second mortgage or a home equity line of credit, you are using your home as collateral. That means if you stop paying, the lender can take your house. But even if you keep making every payment on time, a drop in home value can still cause trouble. Imagine your home is worth three hundred thousand dollars and you owe two hundred thousand on your first mortgage. That leaves you with one hundred thousand in equity. You decide to take out a home equity line of credit for fifty thousand dollars to remodel your kitchen. Now your total debt is two hundred and fifty thousand dollars. Your equity is down to fifty thousand dollars. That still seems safe enough.Then the market takes a downturn. Home values in your neighborhood fall by twenty percent. Your three hundred thousand dollar home is now worth two hundred and forty thousand dollars. But you still owe two hundred and fifty thousand. You owe more than the house is worth. You are underwater. This is also called negative equity.Being underwater does not automatically mean you will lose your home. If you keep making payments, your lender will not take any action. But the problem comes when something changes in your life. Maybe you lose your job, get divorced, or need to move for a new job. You cannot sell your home without bringing cash to the closing table to pay off the difference between what the house sells for and what you owe. That can be tens of thousands of dollars that you may not have.Another problem is that your home equity line of credit may be frozen or reduced. Many lenders have the right to lower your credit limit or stop you from drawing more money if the value of your home falls. That can catch you off guard if you were counting on that money for an emergency or a planned expense. You might have already used part of the line, but the remaining available credit disappears.A drop in home value also makes it harder to refinance. If you want to lower your interest rate or switch from an adjustable rate to a fixed rate, you need enough equity to qualify. When home prices fall, you may not have that equity. You could be stuck with a higher payment or a loan that is about to adjust upward.There is also the stress factor. Knowing that you owe more than your home is worth can feel like a weight. It can affect your decisions about upgrades, moving, or even taking on new debt. Some people panic and try to sell at a loss, while others hold on hoping the market will come back. That wait can last years. In some housing downturns, it took a decade for prices to recover.The best way to protect yourself is to be conservative when using your home equity. Do not borrow the maximum amount you are offered. Leave a cushion. Think about what would happen if your home value dropped by ten or fifteen percent. Would you still have some equity left? If not, you are too close to the edge.Also remember that a home is a place to live, not an ATM. Using your equity for expenses that do not add lasting value, like vacations or a new car, can leave you with debt and no way to pay it back if the market turns. Even if you use the money for home improvements, make sure those improvements actually increase the value of your house by at least as much as you borrow. Not all renovations pay off.Finally, keep an eye on your local housing market. If prices in your area have been climbing fast for a few years, a correction may be overdue. That is not a reason to panic, but it is a reason to be extra careful about how much equity you take out. A downturn can happen quickly, and once you have borrowed against your home, you cannot undo that decision.Leveraging your home equity can be a useful tool. But it comes with real risk. The biggest risk is that home values do not always go up. When they fall, the equity you thought was yours can disappear, and you could end up owing more than your house is worth. That is a situation no homeowner wants to face. By understanding this risk ahead of time, you can make smarter choices about how much equity to use and when.

First-time homeowners often underestimate utilities that were previously included in rent. Be sure to account for: Water and Sewer Trash and Recycling Collection Natural Gas or Propane Increased electricity usage (for a larger space)

This depends entirely on the HOA’s policy for that specific assessment. Some associations may allow you to pay in monthly or quarterly installments, sometimes with an interest or administrative fee. Others may require a lump-sum payment by a specific deadline.

A cash-out refinance makes sense when you have a specific, valuable need for the funds, such as home renovations that increase your property’s value, consolidating high-interest debt (like credit cards), or funding a major investment. It’s crucial to have a disciplined plan for the cash and to understand that you are increasing your mortgage debt.

From the point of formal application to closing, the process typically takes 30 to 45 days. However, this timeline can vary based on the complexity of your financial situation, the type of loan, the lender’s workload, and how quickly you provide requested documentation.

Property taxes are based on the assessed value of your home and the land it sits on. A local government tax assessor determines this value, and the tax rate (or millage rate) is set by local taxing authorities like the city, county, and school district. The tax is calculated by multiplying the assessed value by the tax rate.